• Property sold for: ₹5 Cr

• Purchased in FY 2015–16 for: ₹2 Cr

• Indexed Cost (CII based): ₹2.74 Cr

• LTCG:₹2.26 Cr

• LTCG Tax (@20.8%): ₹47.0 lakhs

• Net amount after tax: ₹5 Cr − ₹47L = ₹4.53 Cr (rounded to ₹4.6 Cr for simplicity)

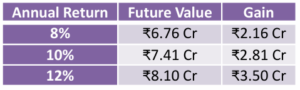

SCENARIO A: Pay Capital Gains Tax & Invest ₹4.6 Cr in Mutual Funds

Future Value at different returns (8%, 10%, 12%) over 5 years

Note: LTCG on mutual fund gains above ₹1 lakh is taxed at 10% (excluding indexation).

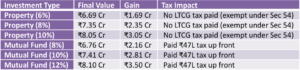

SCENARIO B: Don’t Pay Capital Gains Tax — Reinvest Entire ₹5 Cr in a Property

(Section 54)

Let’s assume:

• Entire ₹5 Cr invested in residential real estate

• Growth rate: 6%, 8% and10% CAGR

• Holding period: 5 years

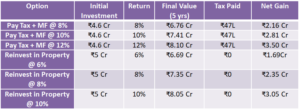

Summary Table

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.