An Employee Stock Option Plan (ESOP) gives you the right (not the obligation) to purchase shares of your company at a pre-determined strike price, after a certain vesting period.

The lifecycle looks like this:

Taxation happens at two key stages – exercise and sale – and potentially every year if dividends are paid. If the company is listed outside India, cross-border rules add another layer.

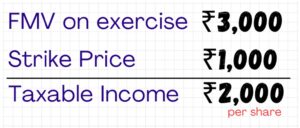

When you exercise your options and receive shares, the first taxable event occurs.

What is taxed?

The difference between:

Fair Market Value (FMV) on exercise date

minus

Exercise price

This difference is treated as perquisite income and taxed as salary.

Example:

This amount is added to your salary and taxed at your slab rate (often 30% + surcharge + cess for senior professionals).

Why this matters

You may owe tax even though you have not sold the shares and received no cash.

If your employer deducts TDS, it will appear in Form 16. If not, you must pay advance tax yourself.

For many professionals, this is the first liquidity strain.

Once you exercise and hold shares, you are the same as any other shareholder. If the company pays dividends, another taxable event arises.

Step 1: US Withholding

US companies withhold tax on dividends paid to non-residents:

- Default rate: 30%

- India–US treaty rate: 25% (if W-8BEN is filed)

Step 2: Taxation in India

Foreign dividends are:

- Taxable under “Income from Other Sources”

- Fully taxed at your slab rate

- Not eligible for concessional rates

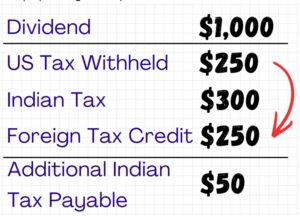

Avoiding Double Tax

To avoid double taxation, you must:

- Declare gross dividend income in India

- Claim FTC for US tax withheld

- Pay only the difference

Example (assuming 30% slab):

Total effective tax equals your slab rate – not double.

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.