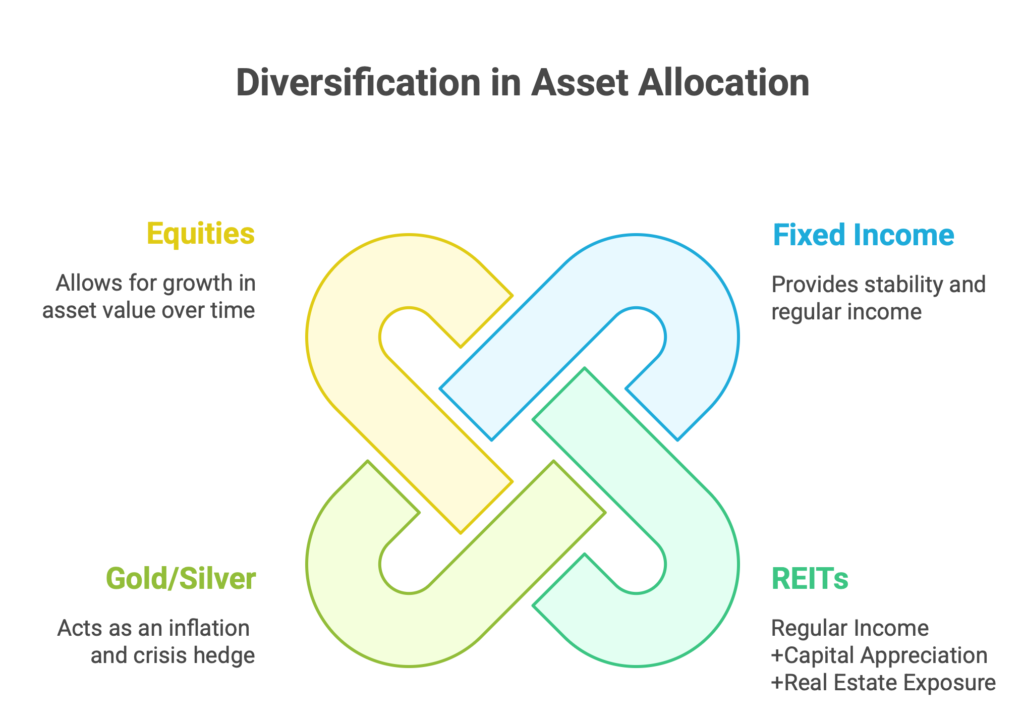

A well-diversified portfolio is one that can sustain different market cycles, as it comprises of asset classes that contribute in different market conditions and offer different risk-reward characteristics. Lower correlation amongst the asset classes helps in diversification.

Not all REITs are created equal. The quality of the underlying assets, tenants, and financial structure can significantly impact long-term returns.

Here are some of the most important metrics and factors to evaluate.

Distribution Yield

The distribution yield is the annual cash distribution paid by the REIT relative to its market price. This is the closest equivalent to a bond yield or rental yield. Indian office REITs typically yield 6–8% distribution yield.

However, yield alone should not drive investment decisions.

Net Distributable Cash Flow (NDCF)

A REIT’s distributions are funded by NDCF – the cash generated from property operations after expenses, interest, and maintenance capex.

Investors should evaluate:

- Growth in NDCF per unit

- Stability of cash flows

- Sustainability of distributions

Consistent growth in NDCF usually indicates healthy rental growth and strong asset performance.

Occupancy Rate

Occupancy is a key indicator of asset quality and demand. High-quality REITs usually maintain 85–95% occupancy levels.

Higher occupancy implies stable rental income and lower vacancy risk.

Persistent vacancy can signal location weakness or high tenant churn.

Weighted Average Lease Expiry (WALE)

WALE measures the average remaining lease duration of tenants.

A longer WALE indicates:

- predictable rental income

- lower tenant turnover risk

Institutional office REITs typically target 4–7 years of WALE.

Tenant Diversification and Quality

Tenant concentration is an important risk factor.

Investors should evaluate:

- exposure to top tenant

- sector diversification

- credit quality of tenants

Many Indian office REIT tenants include global IT companies, consulting firms, and multinational corporations, which reduces default risk.

Acquisition Pipeline

Most REITs are sponsored by large real estate developers or institutional property owners. These sponsors typically maintain a pipeline of assets that can eventually be transferred to the REIT.

Evaluating the pipeline is important as it provides visibility of future growth, scale, diversification benefits and distribution growth.

Releasing Spread (Rental Growth)

Releasing spread measures the increase in rental rates when leases are renewed or new tenants replace existing ones.

Positive releasing spreads indicate strong demand for the property and rising rental markets.

Asset Upgrades and Value Creation

REITs can also increase rental income through active asset management:

- Upgrading building infrastructure

- Improving common amenities

- Reconfiguring office layouts

- Adding retail or service components

These upgrades make properties more attractive to tenants and allow the REIT to command higher rental rates when leases renew.

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.