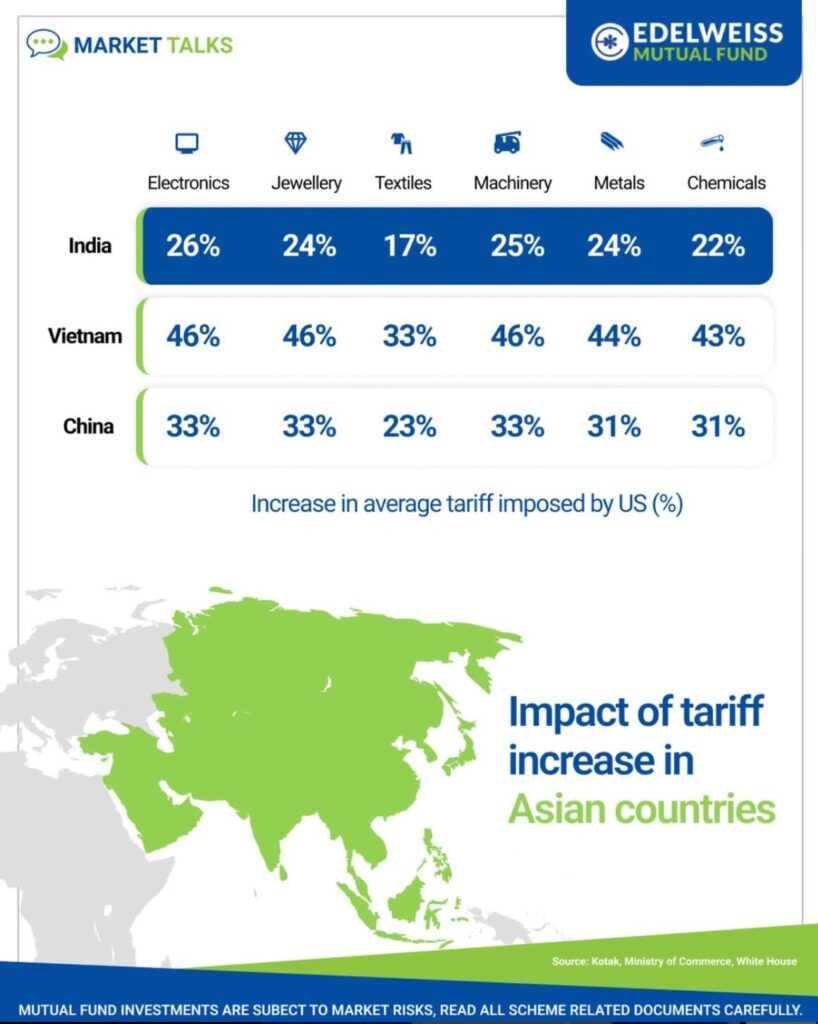

Short-term headwinds like tariffs may lead to supply-side constraints, but it’s important to remember:

- The U.S. accounts for just ~18% of India’s exports.

- It’s not the end of the world.

- In fact, some sectors like textiles and chemicals may benefit from global tariff realignments, thanks to India’s rising competitiveness.

As global dynamics shift, India is on the cusp of a transformative economic journey. Unlike China’s export-led ascent, India’s rise is rooted in domestic consumption, democratic resilience, and a youthful population.

Here are 3 key structural drivers we believe will propel Indian markets forward:

- Domestic driven consumption:

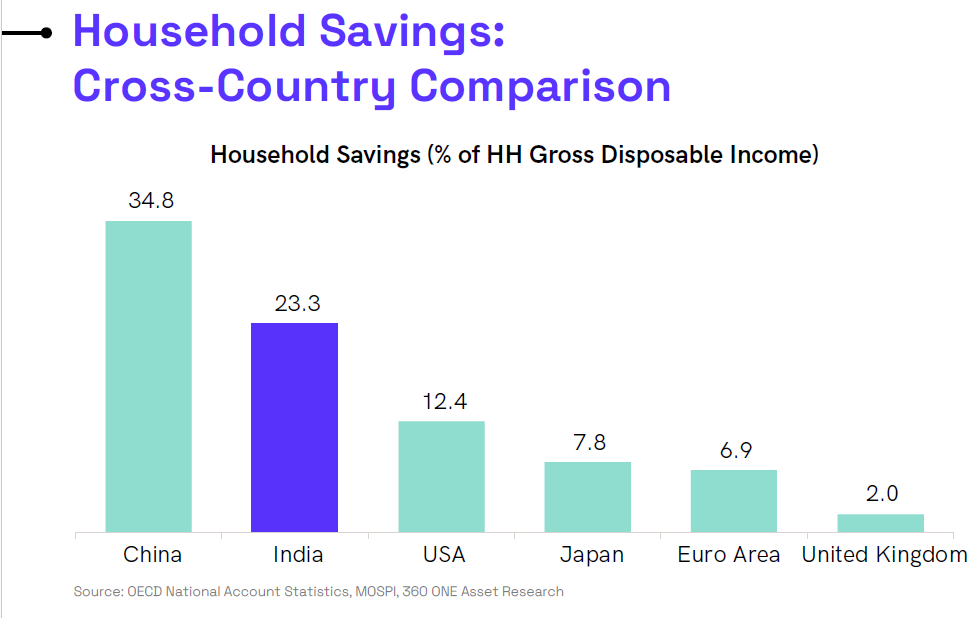

India has one of the highest household savings rates globally.

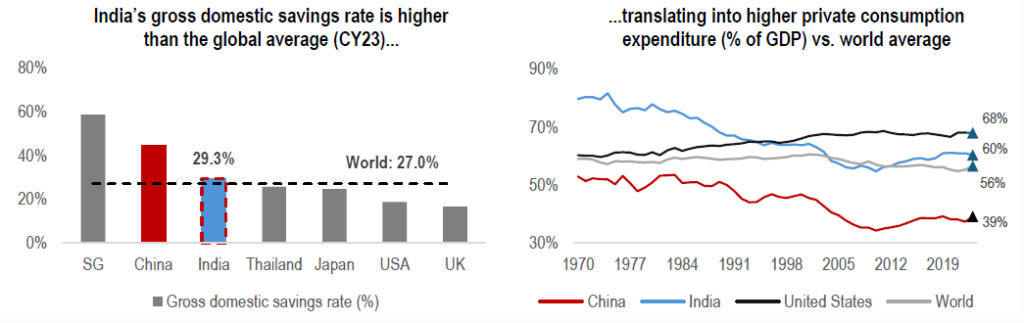

Private consumption, accounting for nearly 60% of GDP, will continue to drive economic expansion. This is in stark contrast to China, where household consumption comprises less than 40% of GDP, reflecting the relative underdevelopment of the consumption sector.

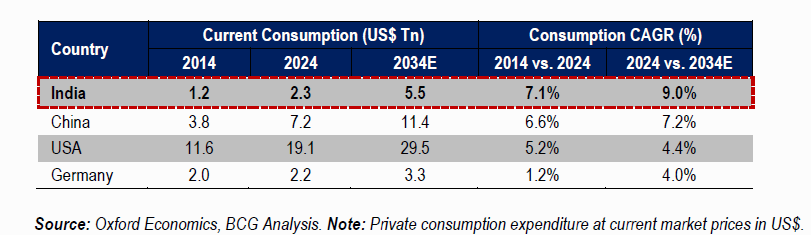

India to witness the highest growth in consumption over the next decade. India’s consumption growth trajectory has been secular and is expected to significantly outpace other major economies, with CAGR growth of 9% (between 2024-34E), followed by China at 7.2% and the US at 4.4%.

Do you know? On what Indian consumers spend more money on?

It is food which is 30% (Per capita Consumption Expenditure) - Govt capex and Infra Development:

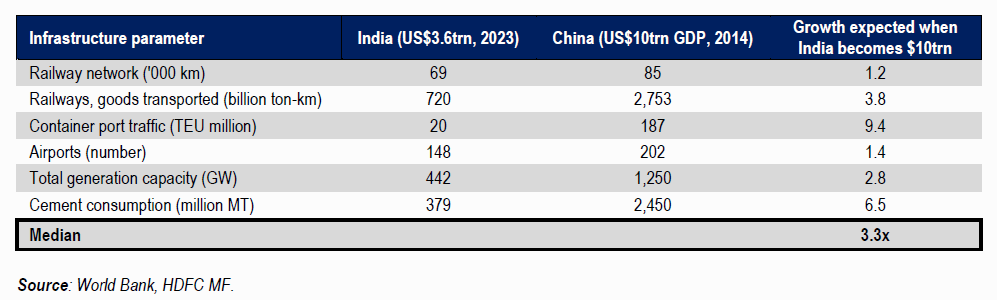

Thanks to robust GST collections, government spending on infrastructure has surged.

We are seeing:

• Faster road and railway construction

• Development of airports

• Increased focus on logistics and connectivity

This will have a multiplier effect across sectors and employment.

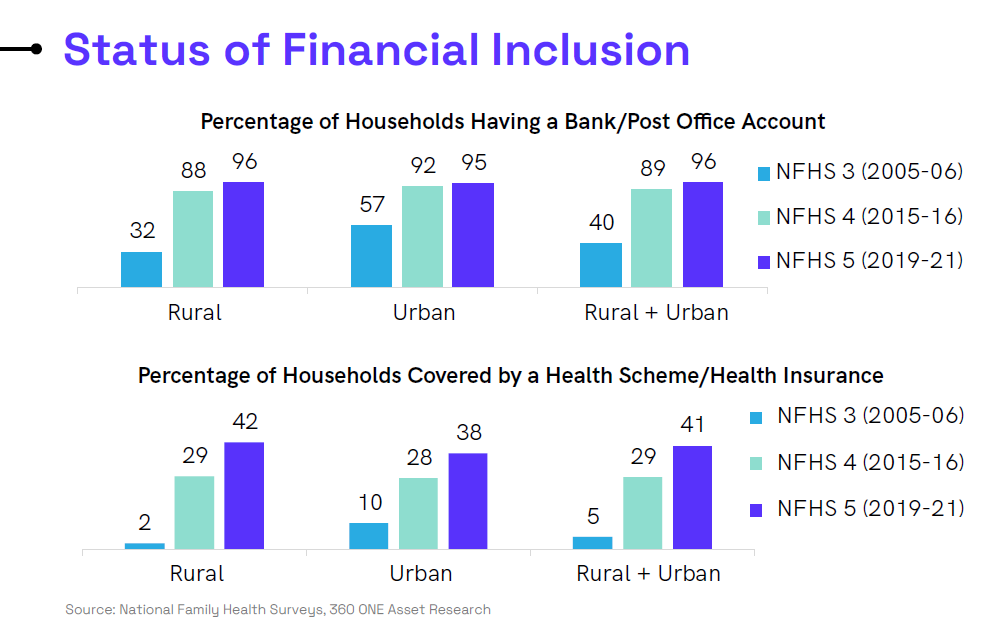

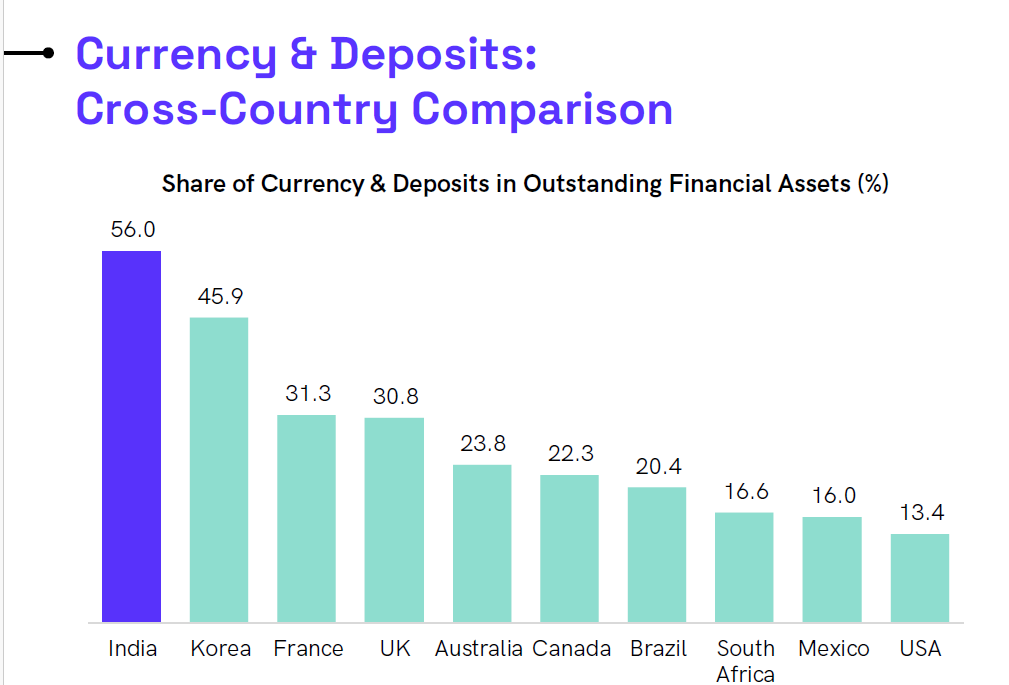

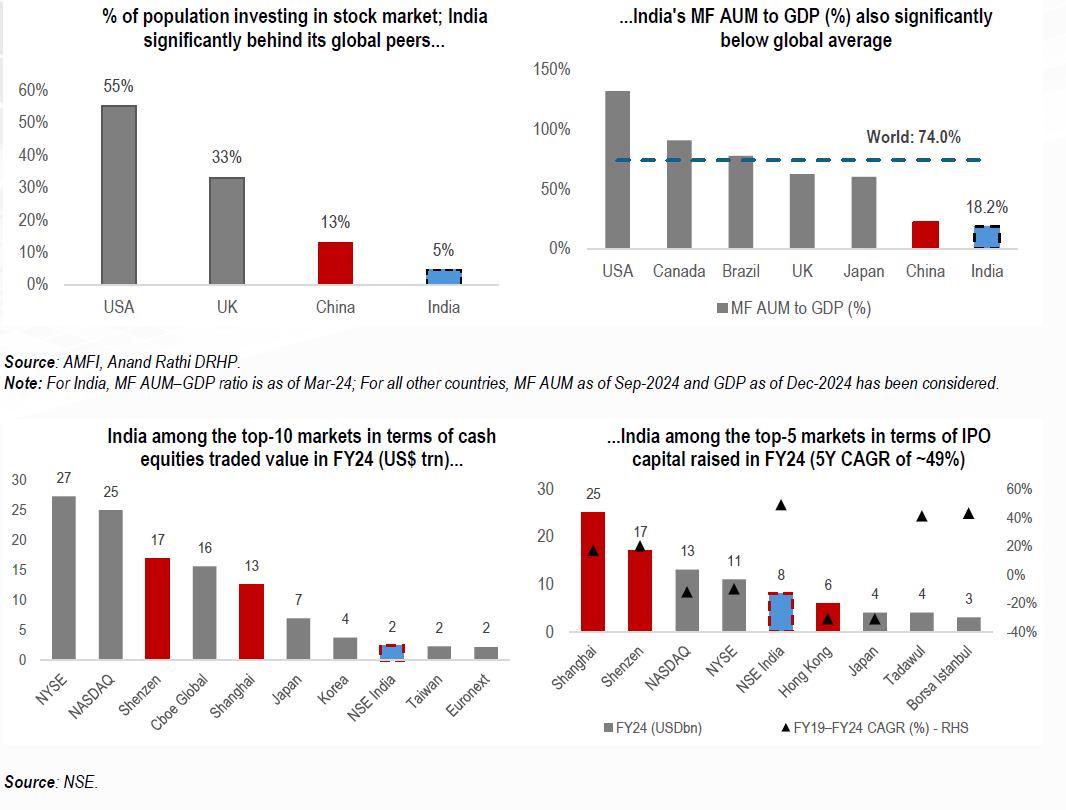

- Financial Inclusion & Equity Participation:Over 98% of the population now has access to a bank or post office account, significantly reducing leakages in government welfare schemes and increasing household participation in formal financial systems.

Yet, India remains underpenetrated in equity ownership relative to global peers. This gap presents a meaningful opportunity:

• As trust in markets builds,

• And digital platforms simplify access to investment products,

• We expect broader retail participation in equities to continue rising

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.