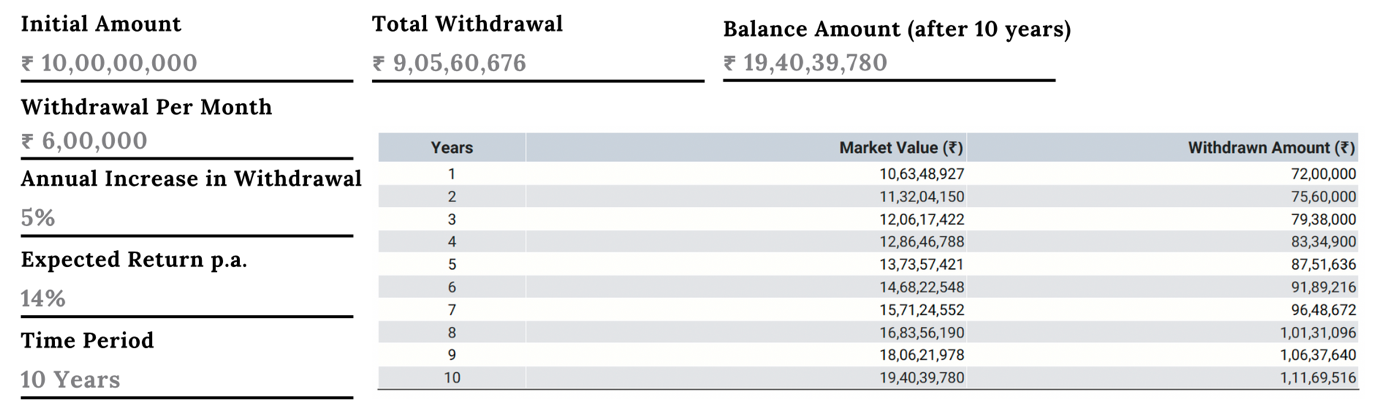

A SWP is a feature that allows mutual fund investors to withdraw a fixed amount from their investment at regular intervals (monthly, quarterly or annually). Instead of redeeming the entire investment at once, a SWP allows for creating a steady and predictable cashflow, while also allowing the remaining corpus to stay invested and reap the benefits of compounding.

The mutual fund house sells enough units at the applicable NAV, to generate the fixed cashflow each period. Alternatively, a SWP can also be set up as a percentage of the corpus, instead of a fixed withdrawal amount.

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.