India needed this reform because its original GST system had become overly complicated. The four-tier structure (5%, 12%, 18%, 28%) created business disputes, compliance burdens, and economic inefficiencies that slowed growth. Many industries faced “inverted duty structures” where they paid higher taxes on raw materials than on finished products, creating cash flow problems.

GST 2.0 consolidates the existing four-slab system into a simplified two-tier structure: 5% and 18% for most goods, with a special 40% rate for luxury and sin goods.

Essential daily-use items move to the 5% bracket, including food products, toiletries, household goods, and agricultural equipment. Consumer durables and automobiles shift to 18%, while luxury cars, tobacco, and alcohol face the new 40% rate.

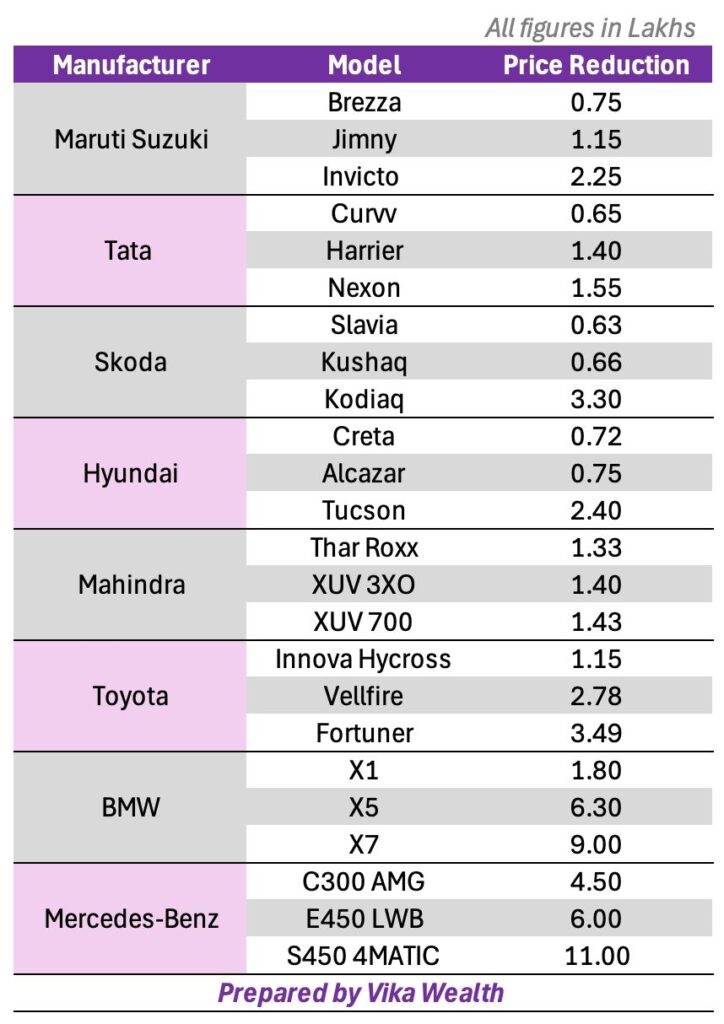

Car Price Reductions Announced by Manufacturers

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.