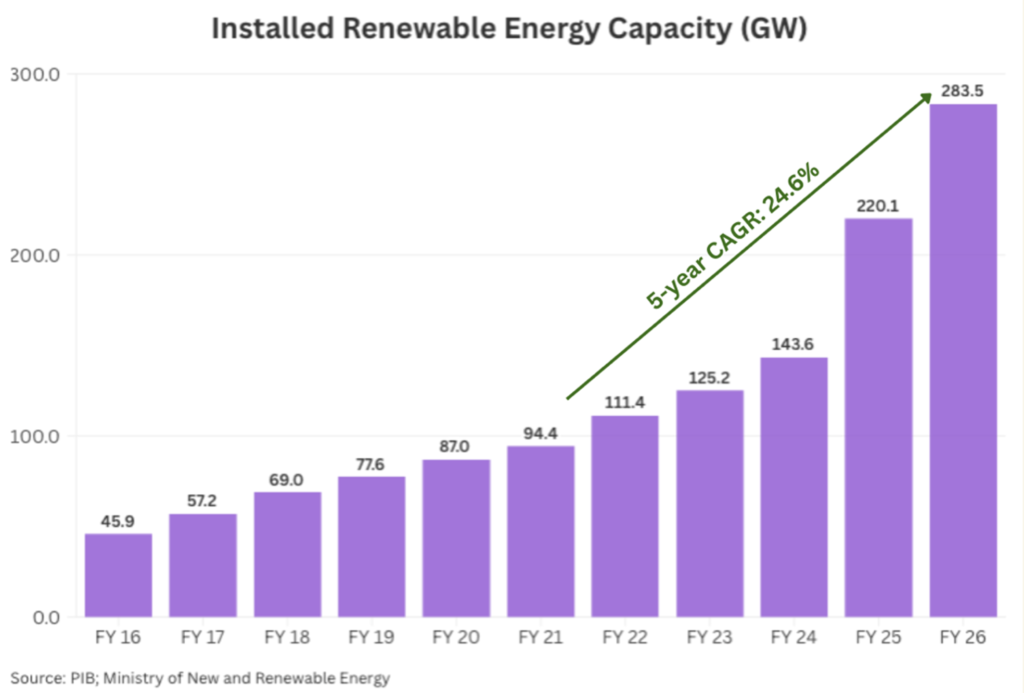

There’s a number that tells you everything you need to know about India’s energy story: 55.3 GW. That’s how much renewable energy capacity India added in FY 2025-26. To put it in perspective, that’s roughly the entire installed power capacity of a mid-sized European country, built in a year.

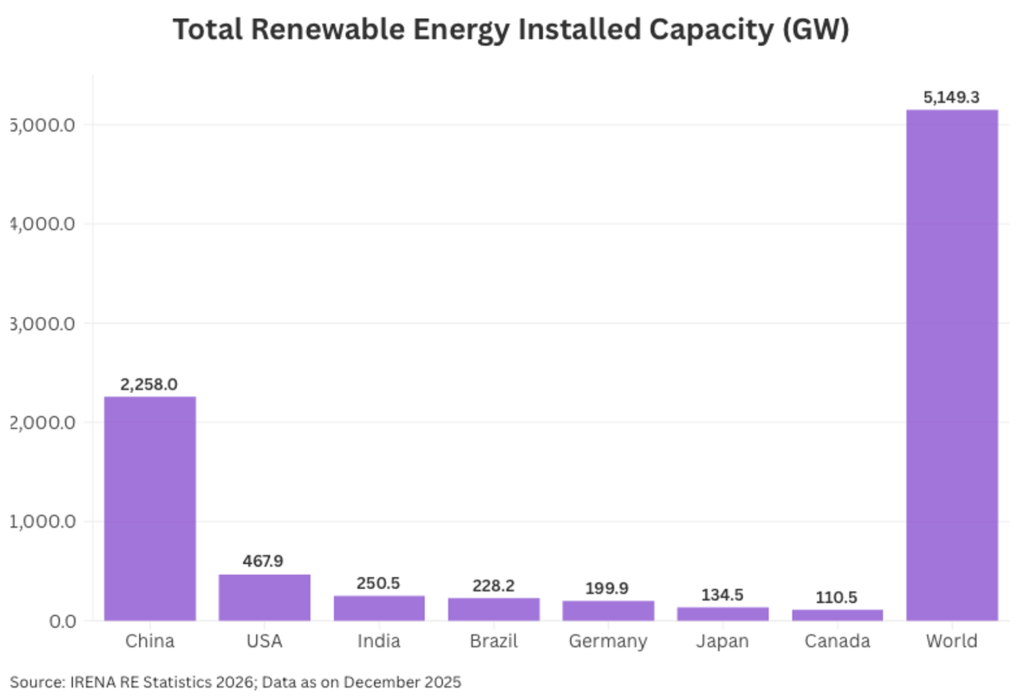

India’s total installed capacity from non-fossil fuel sources stands at 284 GW, which ranks us third globally.

India is not incrementally expanding its clean energy footprint. It is undergoing a structural transformation. For investors, the window to participate is wide open.

India’s Panchamrit commitments at COP26 set an ambitious target: 500 GW of non-fossil fuel capacity by 2030, net zero by 2070. What’s remarkable is that India already hit the interim milestone – 50% of installed electricity capacity from non-fossil sources – in June 2025.

This hasn’t happened by accident. The policy scaffolding is comprehensive and well-funded. The MNRE budget for FY26 was increased 39% year-on-year to $3 billion. The Production Linked Incentive (PLI) scheme for solar manufacturing has catalysed 144 GW per annum of domestic module manufacturing capacity, up nearly 100% in 2025 alone. GST on solar modules and wind turbines was cut from 12% to 5%. The Green Energy Corridor is channelling ₹12,000 crore into transmission infrastructure. Viability Gap Funding is being deployed for battery storage and offshore wind.

The government has, in effect, de-risked the investment case across the value chain – from manufacturing to generation to grid.

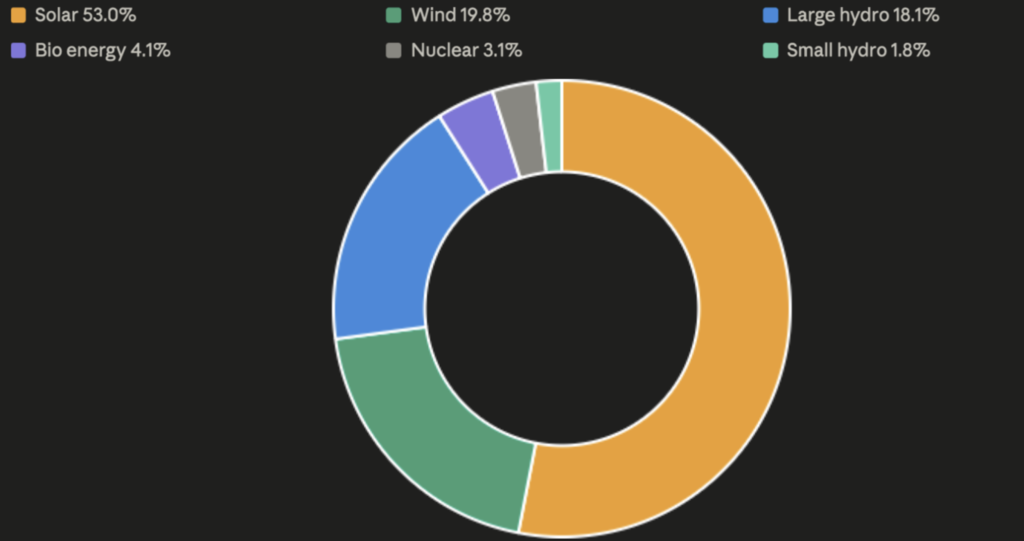

So far, a total of 283.46 GW of capacity from non-fossil fuel sources has been installed in the country as on FY 2025-26 end. This includes 150.26 GW Solar Power, 56.09 GW Wind Power, 11.75 GW Bio Energy, 5.17 GW Small Hydro Power, 51.41 GW Large Hydro Power and 8.78 GW Nuclear Power capacity.

Sri Subhash Yerneni

Sri Subhash is an astute banking and finance professional with 14 years of real-world experience in wealth management, advisory of financial instruments such as mutual funds-equity and debt-alternate investment funds ( AIF)-structure and offshore products-private equity-venture capital/debt-bonds and MLDs-priority banking-cash management-team management-and working with various cultures in various nations.